RESOURCES

Risk-Off… That Was Quick.

U.S. Loan Market Review Q1 2026

Tyler Gramatovich, Vice President, Investments and Portfolio Manager of Invico Capital Corporation’s Credit Opportunities fund, comprised of broadly syndicated loans, provides his commentary on the U.S. loan market in the first quarter of 2026.

Q1 2026 marked a meaningful shift in risk appetite, with sentiment softening as investors reassessed valuations and the pace of change across several sectors, particularly software and technology. While concerns around AI-related disruption are not new, they contributed to a broader repricing of risk and a more bifurcated market environment.

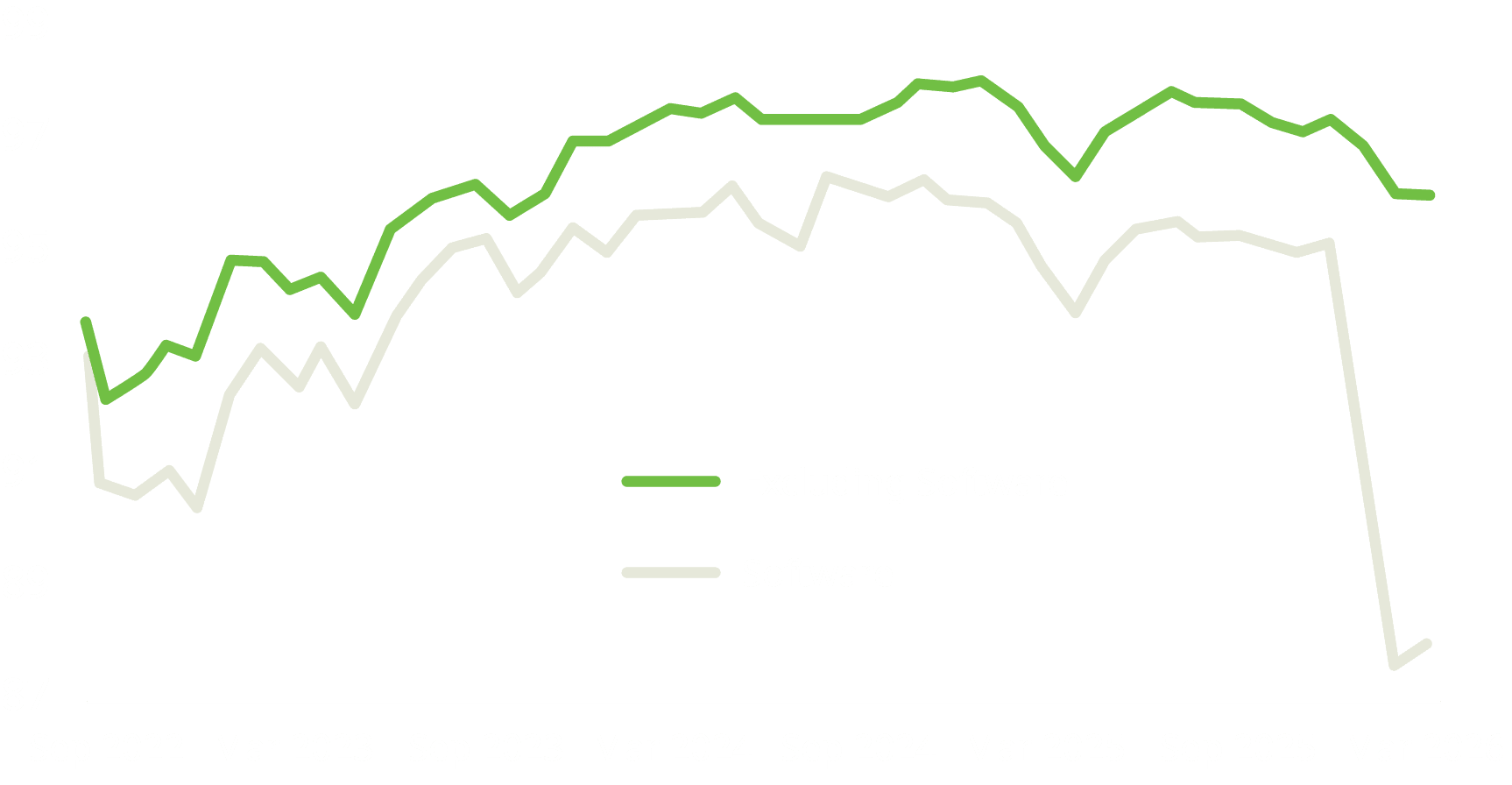

Software was among the first areas to feel the pressure, as post-COVID underwritten loans with higher debt-to-EBITDA multiples came under increased scrutiny. Investors became more focused on business model durability and refinancing risk. In February, the weighted average loan price declined to 94.17 cents on the dollar, falling below the April 2025 “Liberation Day” lows, with software credit contributing meaningfully to the move.

Average Bid Price of Performing U.S. Leveraged Loans

The disruption risk extended across multiple sectors, and a clear divergence has emerged in what the market is willing to underwrite. The loan market slowed but remained open for higher-quality borrowers, while perceived lower-quality issuers were either postponed or punished with a much higher cost of capital. Spreads widened through February and March as markets digested sector-specific stress, geopolitical uncertainty, persistent inflation, and a softer macro sentiment.

Despite this backdrop, conditions continue to favour the first lien, floating rate syndicated loan asset class. Loans were among the more resilient areas of the market during the quarter, underscoring their defensive characteristics in periods of volatility. A senior position in the capital structure, contractual cash flows, and floating-rate exposure remain valuable attributes in an uncertain environment. On an all-in yield basis, current conditions continue to support attractive income profiles, particularly when paired with disciplined credit selection.

While $100+ WTI was not our base case, we have been cognizant of a weakening macro backdrop ahead of recent geopolitical developments. We have remained focused on capital preservation and positioning the portfolio toward resilient, essential businesses with stable capital structures in a no-growth environment. We have been explicit in our shift “up in quality,” and Q1 reinforced the value of that approach, with BB-rated loans outperforming and higher-quality credits demonstrating greater durability in a stressed environment.

| Asset Class Returns YTD through March 31, 2026 | Total Return |

|---|---|

|

S&P 500

|

(4.33%)

|

|

US Treasuries

|

(0.04%)

|

|

US Investment Grade Bonds

|

(0.05%)

|

|

US High Yield Bonds

|

(0.50%)

|

|

Cliffwater BDC Index

|

(9.95%)

|

|

US Leveraged Loans

|

(0.55%)

|

|

US Leveraged Loans - BB Rated

|

0.71%

|

|

US Leveraged Loans - B Rated

|

(0.90%)

|

|

US Leveraged Loans - CCC Rated

|

(4.94%)

|

Source: Bloomberg.

If you would like to learn more about Invico’s syndicated credit strategy and how you can incorporate it into your portfolio, get in touch with our investment sales team.

About Tyler Gramatovich, CFA, PM

Tyler is Vice President, Investments and Portfolio Manager at Invico Capital Corporation, with over a decade of experience in the North American high-yield and leveraged loan market. As Vice President of Investments, Tyler is responsible for originating and analyzing corporate debt investments on behalf of the firm’s managed investment offerings. He also oversees secondary corporate credit investment opportunities, including the generation of investment ideas, conducting fundamental analysis, and executing trades through broker relationships across North America on behalf of the firm.

Forward-Looking Statements

Certain statements or information contained above constitute “forward-looking statements” within the meaning of that phrase under applicable Canadian securities laws. Any statements that express, or involve discussions as to, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, through the words or phrases such as “will likely result”, “are expected to”, “expects”, “does not expect”, “anticipates”, “does not anticipate”, “believe”, “continue”, “estimate”, “intend”, “plan”, “potential”, “predict”, “project”, “seek” or other similar words) are not statements of historical fact and may be forward-looking statements. Forward-looking statements involve Invico Diversified Income Administration Ltd.’s (the “Administrator”) and Invico Capital Corporation’s (the “Portfolio Manager”) internal projections, estimates or beliefs concerning, among other things, future growth, results of operations, investment opportunities, future expenditures, plans for and results of investments, portfolio results, business prospects and opportunities. Although the Administrator and the Portfolio Manager believe that the expectations, estimates and projections reflected in the forward-looking statements are reasonable, they cannot guarantee future results, levels of activity, performance or achievement since such expectations are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies which could cause the Fund’s actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, the Fund. Because of the risks, uncertainties and assumptions contained herein and in the Offering Memorandum, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits the Fund will derive therefrom. Prospective investors should not place undue reliance on forward-looking statements.

Forward-looking statements contained in this document include, but are not limited to, statements with respect to: the use of proceeds of the offering; the business to be conducted by the Fund and the Partnership; timing and payment of distributions; payment of fees and expenses; the Fund’s investment objectives and investment strategies; the Partnership’s active investment approach; the degree of control exerted over management of investee companies by the Partnership; anticipated investments and investment pipeline; the assets to be held by the Partnership; the process by which the Partnership determines whether or not to make an investment; the Partnership’s expected capital investments and objectives with respect to Invico Energy USA and Invico Energy; treatment under governmental regulatory regimes and tax laws; financial and business prospects and financial outlook; the ability of the Fund and the Partnership to redeem units; types of portfolio securities and results of investments, the timing thereof and the methods of funding; anticipated terms of the Partnership’s lending arrangements; the Partnership’s strategies to manage defaults; objectives with respect to “equity yield investments”; and prospects and targets with respect to the offering.