RESOURCES

Volatility to Velocity

U.S. Loan Market Review Q2 2026

Tyler Gramatovich, Senior Vice President, Investments and Portfolio Manager of Invico Capital Corporation’s Credit Opportunities fund, provides his commentary on the U.S. loan market in the second quarter of 2026.

The first half of the year was eventful for risk assets, with the volatility experienced in Q1 2026 giving way to the strongest quarter for equities since the post-COVID rally in Q2 2020. The rebound in risk assets was supported in part by what we view as a fragile peace deal between the U.S. and Iran, though improving investor sentiment was also a meaningful driver of the rally.

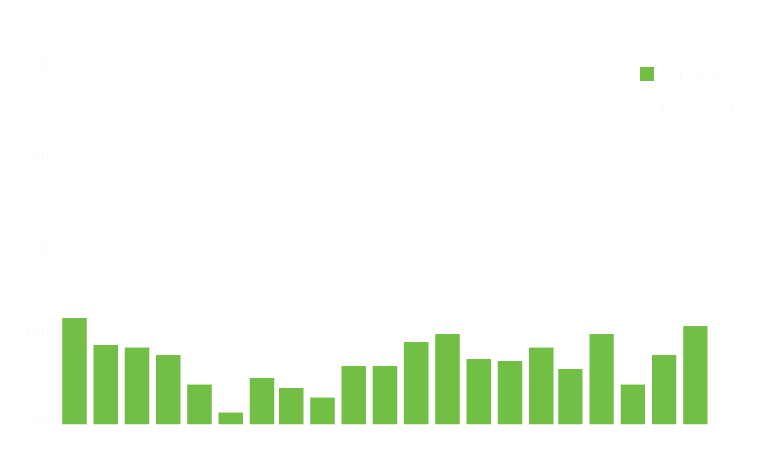

The loan market remained active, resilient, and increasingly bifurcated in Q2 2026, with $221 billion of new loan issuance during the quarter. While spreads for lower-quality borrowers in the B- cohort continued to widen, spreads for higher-quality borrowers in the B and BB cohorts remained relatively stable, reinforcing the view that investors are becoming increasingly selective even in a risk-on environment.

Performance in the loan market was front-end-loaded, with April generating a 1.29% total return, representing nearly all the market’s 1.32% year-to-date gain. June finished essentially flat, as coupon income was largely offset by modest price declines.

U.S. Institutional Loan Issuance ($Bn)

Looking Ahead

The current environment continues to present compelling opportunities for attractive, stable income as we look ahead to the remainder of 2026. As macroeconomic and sector-specific risks converge (from a more hawkish Federal Reserve and energy-driven inflation pressures to growing concerns around AI-driven disruption in software), selectivity remains critical. At the same time, equity valuations remain near all-time highs, leaving limited margin for error should earnings expectations reset lower. In our view, this is an environment where active credit selection and disciplined portfolio management are essential to preserving capital while continuing to capture attractive risk-adjusted yield.

We believe the case for senior secured public credit remains particularly compelling for yield-oriented investors in this uncertain environment. A carefully constructed portfolio of first lien loans, focused on higher-quality issuers and actively managed through disciplined credit selection, can help offer a differentiated combination of capital preservation and monthly income.

With high-single-digit yields, floating-rate protection, and transparent mark-to-market pricing, we continue to view this asset class as one of the most attractive opportunities within fixed income, offering an effective means of protecting capital while generating tangible monthly income.

If you would like to learn more about Invico’s syndicated credit strategy and how you can incorporate it into your portfolio, contact our investment sales team.

About Tyler Gramatovich, CFA, PM

Tyler is the Senior Vice President, Investments and Portfolio Manager at Invico Capital Corporation, with over a decade of experience in the North American high-yield and leveraged loan market. As Senior Vice President of Investments, Tyler is responsible for originating and analyzing corporate debt investments on behalf of the firm’s managed investment offerings. He also oversees secondary corporate credit investment opportunities, including the generation of investment ideas, conducting fundamental analysis, and executing trades through broker relationships across North America on behalf of the firm.

Forward-Looking Statements

Certain statements or information contained above constitute “forward-looking statements” within the meaning of that phrase under applicable Canadian securities laws. Any statements that express, or involve discussions as to, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, through the words or phrases such as “will likely result”, “are expected to”, “expects”, “does not expect”, “anticipates”, “does not anticipate”, “believe”, “continue”, “estimate”, “intend”, “plan”, “potential”, “predict”, “project”, “seek” or other similar words) are not statements of historical fact and may be forward-looking statements. Forward-looking statements involve Invico Diversified Income Administration Ltd.’s (the “Administrator”) and Invico Capital Corporation’s (the “Portfolio Manager”) internal projections, estimates or beliefs concerning, among other things, future growth, results of operations, investment opportunities, future expenditures, plans for and results of investments, portfolio results, business prospects and opportunities. Although the Administrator and the Portfolio Manager believe that the expectations, estimates and projections reflected in the forward-looking statements are reasonable, they cannot guarantee future results, levels of activity, performance or achievement since such expectations are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies which could cause the Fund’s actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, the Fund. Because of the risks, uncertainties and assumptions contained herein and in the Offering Memorandum, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what benefits the Fund will derive therefrom. Prospective investors should not place undue reliance on forward-looking statements.

Forward-looking statements contained in this document include, but are not limited to, statements with respect to: the use of proceeds of the offering; the business to be conducted by the Fund and the Partnership; timing and payment of distributions; payment of fees and expenses; the Fund’s investment objectives and investment strategies; the Partnership’s active investment approach; the degree of control exerted over management of investee companies by the Partnership; anticipated investments and investment pipeline; the assets to be held by the Partnership; the process by which the Partnership determines whether or not to make an investment; the Partnership’s expected capital investments and objectives with respect to Invico Energy USA and Invico Energy; treatment under governmental regulatory regimes and tax laws; financial and business prospects and financial outlook; the ability of the Fund and the Partnership to redeem units; types of portfolio securities and results of investments, the timing thereof and the methods of funding; anticipated terms of the Partnership’s lending arrangements; the Partnership’s strategies to manage defaults; objectives with respect to “equity yield investments”; and prospects and targets with respect to the offering.